Scottish Property magazine

in association with

Words by Ross Walker

Personal Finance Solutions

"If you are in negative equity and need to move home we are here with options for you"

Negative equity occurs when the price of a property falls so dramatically that it is no longer worth as much as the loan that was taken out on it.

This means that the bank or building society no longer has enough security to cover the loan. It is estimated in Scotland that 13% of homeowners are currently in negative equity.

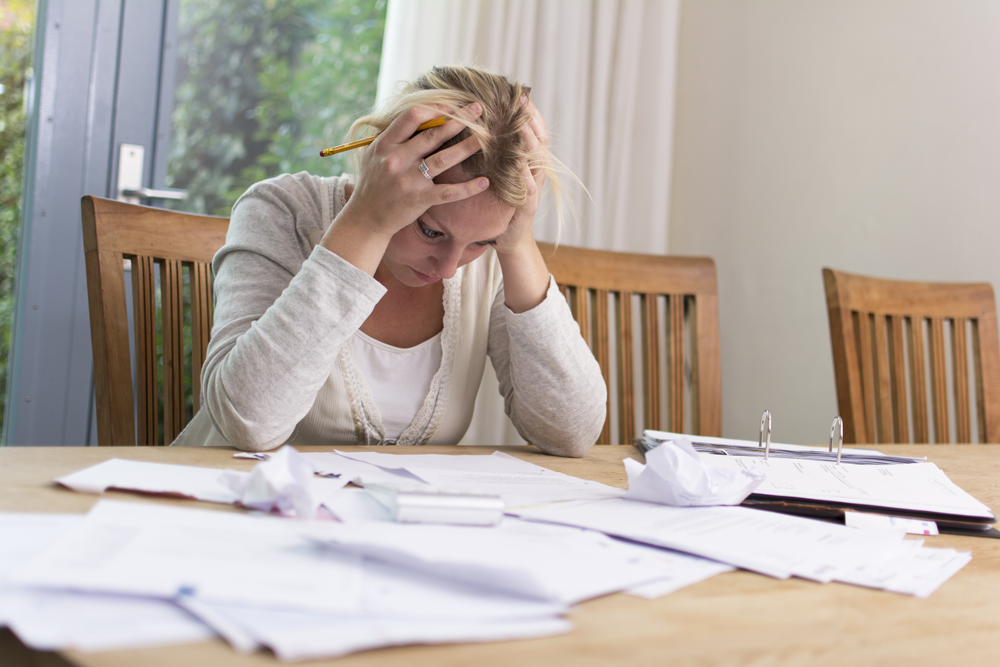

Negative equity, while not a cause for panic in itself, can make things more complicated if you do need to move. This isn't too much of an issue if you can afford to keep up with your mortgage payments and are able to sit out the slump. However, if you do need to move house being in negative equity makes things a lot more complicated.

If you are in negative equity and need to move home, here are your options:

Additional Debt Burden

All too often in addition to negative equity, but not in any way exclusive to just homeowners with negative equity, we see the added complication of dealing with unmanageable and unaffordable unsecured debts which creates a feeling of despair and piles more pressure on already stretched household finances.

Individuals fall into the debt trap for a variety of reasons, normally due to a change of circumstances within the household such as a loss or reduction of household income.

If there is no pressing requirement to move or relocate then considering one of the Scottish statutory debt solutions could be the answer to dealing with the debts allowing control of the finances to be regained and a debt free future with. This would also potentially allow time for the home value to recover.

The statutory solutions available in Scotland are as follows.

| Debt Arrangement Scheme (DAS) | DAS is a government-run debt management tool which allows someone in debt to repay their debts through a debt payment program (DPP). The DPP will allow a debtor to pay off their debts over an extended period of time while giving them protection from their creditors taking action against them to recover the debt in the DPP. The DPP can last for any reasonable length of time and, if approved, will freeze all interest, fees and charges on the debts, resulting in them being written off if the debtor fully completes the DPP. The DAS ignores any assets already owned by the client including property. |

| Trust Deeds | A Trust Deed uses government legislation to enable people living in Scotland, who are struggling with unmanageable debts, generally £5000 or more, to manage their debts within a realistic timeframe. The duration of the repayment period is typically 48 months and you will pay an agreed monthly contribution based on your affordability, and once completed, all of your remaining debts are legally written off. This is set up as a voluntary agreement between yourself and the people that you owe money to (your creditors) and is best suited for people who have a regular income and who are able to commit to a repayment schedule which will become legally binding. The added advantage is that once it is agreed (becomes Protected) this prevents your creditors from adding further interest and charges and also from taking any further action against you. The process, from start to finish is handled by your trustee (an insolvency practioner), who organises the paperwork , deals with the creditors on your behalf and manages the process to completion. |

| Sequestration (Bankruptcy) | Sequestration is the Scottish term for Bankruptcy. In 2008 the laws relating to Scottish Bankruptcy were changed allowing debtors to apply for their own bankruptcy, rather than having to wait for a creditor to do so. If you owe £1500 or more, you can apply for your personal bankruptcy. The process is similar to that of a Trust Deed and is handled by a trustee. In both Trust Deeds and Sequestration existing assets such as your property are taken into account by your trustee (the person who administers your Trust Deed or Sequestration) and a valuation is sought prior to going ahead with the solution. If after the valuation is carried out there is little or no negative equity then your trustee will confirm in writing that they have no interest in your property and it will be unaffected by the Trust Deed or Sequestration. |

Editor's Note

The general consensus is that the Scottish housing market is in recovery, but the view remains mixed at regional and local level. What a homeowner does about negative equity really depends on what is priority and what is needed as opposed to desired. A homeowner who is struggling to pay the mortgage and falling further in debt requires a different approach to someone who may be managing mortgage payments and has landed in negative equity due to the fall in house prices. One needs a more urgent solution than the other. If homeowners have free disposable income, making overpayments now to help reduce the negative equity gaps would be a very sensible course of action. Lenders may also want to be more flexible with the terms and conditions placed on mortgages, allowing customers to overpay without facing fines. Always seek advice from a professional when considering selling your home or dealing with debts.

Contact: rosswalker@pf-solutions.co.uk / 0845 302 4628

Newsletter - if you enjoyed this article, why not get more?

Fresh, tasteful, inspiring and brand new, Scottish Property Magazine offers sixty eight tantalising pages filled with beautiful photographs, inspirational ideas and in-depth articles on the following themes:

For the first four editions we are doing direct targeted distribution. The magazine is sent to 10,000 homeowners across the greater central belt, all of whom are either planning to sell, have just sold or have just bought a property. This strategic distribution will continue next year, however, we will also have it in the shops for sale by next summer. A smaller number also gets distributed to IFA's and brokers across the central belt.

Share on facebook

Share on facebook Tweet article

Tweet article Share This article

Share This article +1 This Article

+1 This Article